Fantasy:

"Interbank borrowing costs — a much-watched gauge of the trust banks have in each other — rose to a 10-month high this week, unsettling investors, but many blame the problem mainly on a shortage of dollars in the system rather than outright fear of a bank counterparty failing."

—"Markets Fret, but Chance of Big Bank Crash Slim" (Reuters, 5/28/2010)

Reality:

"I believe finance has tightened and this ... will not prove fleeting.

"...The waves of liquidity unleashed through speculator leveraging and the flight out of safehaven assets has run its course. As we’ve seen over the past few weeks, markets can go from seemingly over-liquefied to illiquid the moment speculators reverse course and head for the exits.

"...The markets have passed an important inflection point, and faltering markets are certainly not good for fragile confidence."

— "Unwitting Beneficiary?" (Credit Bubble Bulletin, 5/28/2010)

That "shortage of dollars" bit from Reuters is hysterical ... not as in funny, but as in panicked.

And that story's headline is not exactly a confidence booster. If recent history is any guide, such is the language used when risk of a big bank crash has become astronomical and, indeed, imminently threatening.

They say, "time will tell." The more I see, the more I agree with Richard Russell. By the end of the year we might not recognize the place.

Circle June 9th on your calendar. That's the day Congress begins deciding the fate of that mountain of casino chips otherwise called OTC derivatives. Being in the bailiwick of the British offshore banking system, how anything combining the words "British" and "offshore" might not quickly conjure images of disaster is a thought worth pondering as election day draws nearer.

Bear in mind, too, the hacks will be conferring immediately following their Memorial Day recess. Chances are the urge to strengthen a terribly weak "reform" bill might be overwhelming once the rage of constituents back home is felt, acting like a torpedo threatening to sink any hope for reelection. Thus, too, the risk of another market dislocation brought on by a threat whose codename is "Glass-Steagall" remains very real.

Probably the more likely scenario, though, is the hacks bleed financial industry lobbyists and fill up their campaign coffers, then put together a bill that is sure to be voted down.

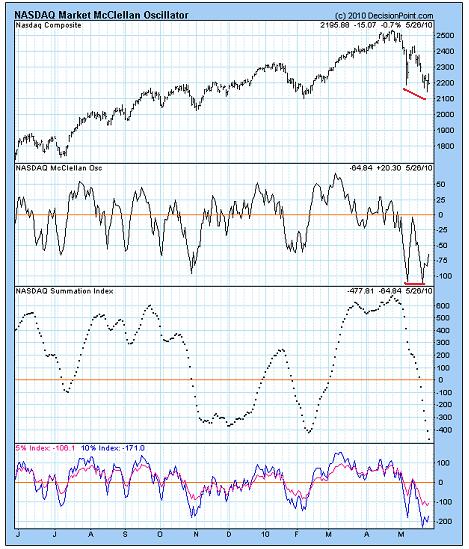

From top to bottom each panel reads: weak, weak, weak, and weak.

RSI, firmly on the sell-side ... the index being turned away from its 200-day moving average ... following a bounce on volume demonstrating a case of George Costanza shrinkage ... leaving momentum (MACD) still firmly in the negative.

All not good. Now, this is a problem we can blame mainly on a dollar shortage!

The coming holiday-shortened week might be punctuated by relatively dull trading. In fact, the post-May 6th bounce, as well as that beginning on Friday, May 21st, could offer a reasonable sense of what to expect. Following a sharp drop into a bottom and a strong subsequent recovery in both instances, a slow grind into a top set the stage for the next leg lower. So, presently, it appears a slow grind remains in store as wave iv of 1 [down from late-April top] moves toward its completion.

Not sure what to make of gaps highlighted by the line drawn above. In the slow grind higher over coming days this could be an area where support develops.

(Looking forward, this line might prove upside resistance in the formation of wave 2. At the moment it appears something of a line in the sand is being drawn here. Yet once this line is taken out over the next couple weeks, today's [meager] support might prove tomorrow's [defeated] resistance.)

Possibly toward the end of the coming, holiday-shortened week, the market's anticipated final leg lower — slated to end but the first wave down from late-April top — will begin commencing. This pending decline could sink the S&P 500 to the 950-1000 area. Furthermore, much like occurred this past Tuesday (May 25th), and then on May 6th before that, bottom could be reached intra-day, and be followed by a screaming recovery.

This is how bottoms have developed thus far anyway — in the process demonstrating a "Save Our Ship" mentality one might reasonably expect at this early moment in a massive decline yet to come. "Like from like" behavior has a way of subtly presenting itself during related moves, as I recently mentioned.

Judging by improvements in the condition of various "oversold" technical measures presented here this week (and the fact these measures continue confirming the market's weak state), one can conclude there exists reasonable basis for anticipating a final leg lower in the formation of wave 1 down from late-April top. During this pending decline likely developing will be such technical divergences as pave the way for formation of wave 2.

(p.s. I added some remarks to yesterday's post in response to Doug Kass' observations on fear, because the technical case against his calling March '09 lows a "generational bottom" trumps his expressed sense about what makes for a rational buyer of stocks here.)

(p.p.s. Returning to "fantasy" and "reality" quoted at the start... Is not a "shortage of dollars in the system" in fact a reflection of collapsing confidence in said system's integrity?)

* * * * *

© The Risk Averse Alert — Advocating a patient, disciplined approach to stock market investing. Overriding objective is limiting financial risk. Minimizing investment capital loss is a priority.

Analysis centers on the stock market's path of least resistance. Long-term, this drives a simple strategy for safely investing a 401(k) for maximum profit. Intermediate-term, investing with stock index tracking-ETFs (both their long and short varieties) is advanced. Short-term, stock index options occasionally offer extraordinary profit opportunities when the stock market is moving along its projected path.

Nothing is set in stone. Nor is the stock market's path of least resistance always known. More often than not, there are no stock index option positions recommended.

There's an easy way to boost your investment discipline...

There's an easy way to boost your investment discipline...Get Real-Time Trade Notification!

{kind=link}